In the last three posts discussing AI agents in telco, I laid the intellectual runway. We unpacked what agentic AI really is, exposed how different vendors spin the term, and showed why ontologies are the missing Rosetta Stone for every brittle BSS/OSS integration.

Now it is time to move from excitement to execution. This post is your practical game plan. We will drill into the foundations you must have in place, weigh-up the classic build‑versus‑buy dilemma, harvest lessons from early adopters, and finish with a phased roadmap that your board can sign off next quarter.

Foundational prerequisites for AI agent success

Agentic AI will only perform as well as the operational foundations underneath it. Before any proof‑of‑concept graduates to production, telecom leaders must resolve three systemic prerequisites: trustworthy data, friction‑free access, and an elastic Gen AI runway.

- Data quality and context. Every decision the agent makes is a statistical bet based on the evidence you feed it. In most CSPs that data is scattered across dozens of systems, each with its own primary keys, timestamps, and naming quirks (“voice‑prepaid”, “Prepaid‑Voice”, and “MOC” all point to the same product). Common failure modes include: mismatched subscriber IDs between CRM and billing, orphaned network events, and incomplete order histories caused by batch ETL delays. Fixing this requires rigorous data governance:

- Master data management to converge customer, service, and resource identifiers.

- Lineage and data contracts so every upstream change triggers schema tests before it hits production.

- Shared Information and data model that maps entities and relationships in a machine‑readable graph. The ontology becomes the agent’s “mental model”, eliminating the free‑text lookup hacks that cause hallucinations.

- Accessibility. Agents need real‑time, fine‑grained access to that curated knowledge—CSV drops or overnight extracts do not cut it. Low‑latency access is usually blocked by two issues: proprietary interfaces and security blast‑radius fears. Proven remedies include:

- TM Forum Open APIs or GraphQL façade layers to normalize interaction patterns across BSS, OSS, and network controllers.

- Zero‑trust API gateways that enforce OAuth scopes, rate limits, and consent checks so the security team sleeps at night.

- Vector stores (e.g., OpenSearch, Pinecone) populated by event‑driven pipelines that push updates in seconds, enabling retrieval‑augmented generation (RAG) without stale data.

- Flexible GenAI platform. Model velocity is outpacing traditional telco procurement cycles; locking yourself to a single LLM or on‑prem GPU cluster is a future technical debt. The platform should:

- Support multiple model families (OpenAI, Anthropic, Gemini, Perplexity, Llama as well as several others) behind a common abstraction so you can A/B performance and optimize costs.

- Autoscale inference on‑demand GPUs/TPUs—Bedrock, Vertex, or your own Kubernetes fleet—matching peak traffic without stranding capital.

- Isolate workloads with per‑tenant VPCs and encrypted checkpoints so regulated data never leaves the operator’s security perimeter.

Cross‑cutting all three pillars is governance & safety: automated red‑teaming, run‑time policy checks, and explainability logs that let auditors reconstruct every action an agent took. Treat these controls as code in the CI/CD pipeline; if they are optional, they will be skipped under deadline pressure.

| Pillar | What “Good” looks like | Common pitfalls |

|---|---|---|

| Data quality & context | Single Telco Ontology Normalized IDs Clear lineage | Siloed schemas Manual mappings Hallucinated outputs |

| Accessibility | Role‑based APIs Secure vector store Consent checks | FTP drops Proprietary interfaces Hand‑cranked extracts |

| Flexible Gen AI platform | Cloud native Multi‑model TMF open APIs | On‑prem GPU cluster Vendor lock‑in Fixed LLM choice |

| Governance & safety | Red‑teaming Explainability logs SOC2 scope | Shadow IT pilots Weak guardrails Audit gaps |

Strategic considerations – build or buy?

Deciding how to bring AI‑agent capability into your operation starts with a clear-eyed audit of conditions on the ground—because most telecom environments are anything but greenfield. Five practical lenses guide the build‑versus‑buy call:

- System fragmentation and data gravity. Legacy BSS/OSS estates are littered with siloed catalogs, duplicate identifiers, and brittle ETL glue. When heterogeneity is extreme, buying an ontology‑powered overlay that abstracts the mess delivers value months faster than a ground‑up build.

- Talent economics. Gen AI engineers and graph architects are scarce and command premium salaries that vary widely by region. Operators in high‑cost markets may find platform licensing cheaper than assembling a 30‑person AI squad; those with captive low‑cost centers might lean toward building.

- Strategic differentiation vs. time-to-market. If the capability under discussion is your competitive edge—say, intent‑based slice monetization or proprietary rating logic—owning the full semantic model and agent code might make sense. However, as with most competitive differentiators, speed is of essence, tilting the scale toward buy.

- Solution availability and integration risk. If a vendor already offers a packaged control plane, telco ontology, and compliance tooling for your specific use case, buying can shrink deployment from quarters to weeks. When the catalog is empty—or only partly fits—building is likely the only viable path. Pre‑certified solutions also hedge schedule risk when regulators or marketing teams have immovable launch dates.

- Budget structure. Capex‑heavy programs are tough sells in cost‑conscious boards. An OPEX‑friendly subscription model may fit financial governance better, whereas operators flush with spectrum‑auction cash might prefer an asset they can depreciate.

Viewed through these lenses—estate complexity, talent cost, differentiation need, time pressure, solution availability and budget appetite—operators naturally gravitate to one end or the other of the continuum. Carriers scoring high on differentiation and with affordable talent often build. Those staring at launch deadlines or talent shortages buy.

Build – own everything

Building means you craft—not just consume—the semantic layer, tool‑chain, and governance envelope. Telstra’s journey illustrates why a carrier might make that call. Facing a heterogeneous RAN and transport estate, Telstra discovered that no commercial knowledge graph could express mobile, fixed, IT, and customer data in a single, queryable model. Starting in 2021, a cross‑functional crew of about forty specialists—data architects, graph engineers, ML ops—spent two years extending TM Forum’s SID with thousands of Telstra‑specific classes. The result is a “knowledge plane” that feeds closed‑loop assurance and slice monetization. Analysts put the capital envelope at roughly USD 20–30 million, but Telstra now owns the digital twin at the heart of its network strategy. Mark Sanders, Telstra’s chief architect and head of autonomous networks, discussed this with DR (Danielle Rios) in a recent Telco in 20 episode:

T‑Mobile picked a different but equally demanding domain: customer care. Its IntentCX program, announced in late 2024, couples OpenAI models with billions of historic support interactions—without a unifying telco ontology. Every legacy system—from billing to IVR—requires bespoke adapters and prompt tweaks. Early feedback from insiders cites thirty‑plus FTEs and an eighteen‑month runway before first revenue impact. IntentCX proves you can build without an ontology, but each missing semantic bridge reappears later as integration toil.

What building really involves. Standing‑up a GenAI‑capable MLOps stack—this may be a managed service such as Amazon Bedrock, Azure OpenAI, or Vertex AI, or a self‑hosted Kubernetes cluster with GPU/Inferentia nodes—plus hardening data‑contract tests, maintaining red‑team pipelines, and accepting a year or more of negative cash‑flow while the knowledge fabric takes shape.

Buy & overlay – plug in a ready‑made Telco Ontology

When calendar pressure, talent scarcity, or estate complexity make building impractical, adopting an ontology‑centric control plane can vault you from pilot to production in weeks. You fast-track three layers at once: the telco‑specific semantic model, the multi‑agent orchestration layer, and built-in safety tooling. Your team stays in control—mapping source systems and crafting prompts—while the platform takes care of the infrastructure.

A commercial telco‑knowledgeable agentic AI solution such as BSS Magic, arrives with an AI-driven Telco Ontology layer that leverages and extends TM Forum’s SID. It includes pre‑built connectors for common BSS/OSS stacks, and guardrails are baked in. That short‑circuits months of schema design, GPU pipeline plumbing, and red‑team hardening, while avoiding the escalating salaries for GenAI talent in hot markets.

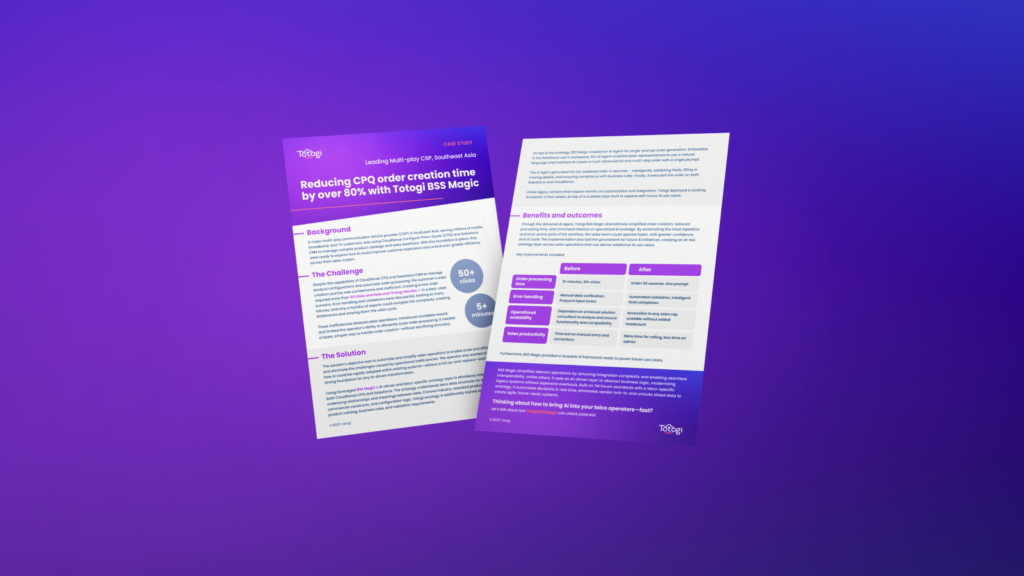

Totogi’s BSS Magic shows how quickly an overlay can translate into measurable impact. A leading Southeast Asian multiplay CSP layered the service on top of its CloudSense and Salesforce estate; within four weeks, the AI agent collapsed a 50‑click, 5‑minute order journey into a single prompt that completes in under 50 seconds. Automated validation eliminated most input errors, any sales rep—not just a trained solution consultant—can now place orders, and reps spend the reclaimed time on selling instead of admin.

The same overlay powered a Tier‑1 North American carrier to shift three million postpaid subscribers off a legacy billing system and onto a cloud SaaS alternative in just 14 days—an exercise its incumbent SI had scoped at nine months. Instead of hand‑coding TM Forum mappings, the carrier simply used BSS Magic’s SID‑aligned adapters, and let the platform auto‑generate the API façade.

In both scenarios, the operators skipped schema design, GPU pipeline plumbing, and bespoke guardrail code. Their teams focused on wiring source systems into the vendor’s ontology and iterating on prompts that reflected their brand voice.

What buying really takes. Clean, well‑documented APIs to feed the vendor’s ontology end executive muscle to drive process change. Capex is minimal and breakeven often arrives within a single fiscal quarter thanks to sub‑minute order times, automated validation, and head‑count neutrality.

| Path | Scope | Time -to-value | Long-term agility | Cost curve | Examples |

|---|---|---|---|---|---|

| Build | Crown‑jewel network or BSS | 12-24 months | High (you own code & knowledge graph) | Capex heavy; opex rises with model ops | Telstra, AT&T, T‑Mobile |

| Buy | Horizontal BSS processes | 4-12 weeks | Moderate (vendor roadmap) | Subscription + usage | Southeast‑ Asian Multiplay CSP, Tier‑1 NA |

Operational and business value

Agentic AI is a profit lever. Whether you build or buy, the economic upside shows up in four places:

- Speed to revenue. Buy‑overlay projects hit production in weeks; build programs take longer but deliver greater differentiation when there are no commercially available telco-knowledgeable agentic-AI solutions and scale-economics support such a decision.

- Escape from legacy constraints. Wrapping yesterday’s apps in SID‑aligned Telco Ontology turns million‑dollar change requests into prompt edits. Operators report 30–50 percent cuts in integration OPEX within the first six months.

- Workforce leverage. An AI‑augmented engineer orchestrates what once required a ten‑person SI squad. Reps freed from order admin spend time cross‑selling, lifting ARPU instead of headcount.

- Experience delta. Predictive care, zero‑touch moves, and intent‑based offers drive higher NPS and lower churn—soft metrics that harden into EBITDA over time.

Conclusion

AI agents are rewriting telecom operations today. Two viable paths exist:

- Build when the capability is core IP, no viable commercial solution available but talent costs and business case allow. Own the ontology, accept a longer runway, harvest deep automation later.

- Buy when speed, talent scarcity, or budget favor a turnkey overlay. Leverage a pre‑built Telco Ontology and measure ROI this quarter.

Totogi’s BSS Magic offers the second path out of the box, letting you focus on product strategy rather than plumbing. But whichever route you take, the winning formula is the same:

- Clean and model your data.

- Wrap it in open APIs.

- Launch a tightly scoped pilot.

- Instrument everything and iterate.

- Scale only what moves the P&L.

Ready to move from hype to hands‑on? See it in action and launch your first telco‑grade agent before the next board cycle.